Investing For Wealth Preservation And Growth

A Guide for High Net Worth Individuals

The responsibility of managing wealth effectively becomes more crucial for high net worth individuals (HNWIs), as maintaining and growing larger sums requires strategic thinking. Unlike the average debt consumer, HNWIs should seek to balance between preserving their wealth, growing it over time, and managing the risks that come with different investment choices. In today’s financial landscape, successful wealth management revolves around understanding risk appetite, diversifying portfolios, and exploring unique investment opportunities. Private lending to property developers is one of many ways to diversify your investment portfolio.

In the UK, high net worth individuals are typically defined as those holding significant financial assets valued at over £1 million, excluding their primary residence. This definition is commonly used by wealth management firms, financial institutions, and tax authorities when assessing the financial status and investment needs of individuals.

However, as of 17th May 2024, the rules for an individual choosing to self-certify to be classified as high net worth for exemption from the normal financial promotions restrictions deemed by the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, were reverted after raising the bar earlier on in the year.

By self-certifying, you can declare on signed documentation that your circumstances meet at least one of two conditions to be treated as a high net worth individual, essentially declaring that you can afford the potential risks associated with certain investment opportunities that are promoted to you. The conditions are if you have in the last financial year:

- received an annual income of £100,000 or more, which does NOT include any one-off pension withdrawals, and or,

- had net assets of £250,000 or more which do NOT include: your home (primary residence), any loan secured on it or any equity released from it; your pension (or any pension withdrawals) or any rights under insurance contracts. Net assets are total assets minus any debts you owe.

Self-certification as a high net worth individual means that you can receive financial promotions where the contents may not comply with rules made by the Financial Conduct Authority (FCA). You are also declaring that if you choose to enter any investment arrangements, that you understand that you can expect no protection from the FCA, the Financial Ombudsman Service or the Financial Services Compensation Scheme.

It is then your responsibility to seek advice from someone who specialise in advising on investments if and where you feel necessary because frankly, no investment activity is 100% safe and you could lose some or all of the money you invest.

This article explores the key aspects of diversifying an investment portfolio and how HNWIs can utilise them to strengthen their overall wealth management strategies.

Real Wealth: The Importance of Investing For Wealth Maintenance And Growth

Wealth preservation is the primary goal for many HNWIs. However, maintaining wealth isn’t simply about keeping it intact - it involves protecting its real value against inflation, currency fluctuations, and economic downturns. To this end, investing plays a critical role.

Inflation, for example, can silently erode wealth over time, diminishing purchasing power. If your assets are not growing at a rate that outpaces inflation, the real value of your wealth diminishes. Investing in diversified assets that yield returns greater than inflation helps protect and even grow wealth over the long term. Additionally, market fluctuations and interest rate changes also require strategic investing to safeguard wealth and maintain liquidity.

The second objective for many HNWIs is growing their wealth over time. This involves making calculated investments that provide returns higher than safer alternatives like cash savings or bonds. While riskier, investing in equities, private equity, or alternative investments has the potential for significantly higher returns. Successful HNWIs actively pursue wealth growth while simultaneously mitigating risks.

Self-Assessing Your Risk Appetite

Before diving into any investments, it’s essential for HNWIs to assess their risk appetite, which refers to the amount of risk you are comfortable with taking on while investing. Understanding your risk profile helps determine the appropriate asset allocation and investment strategies for you individually.

Questions To Help Self-Assess Your Risk Appetite:

- What are your financial goals? Are you looking to maintain your current lifestyle, leave a legacy, or grow your wealth significantly? Defining clear goals will help guide your investment strategy and keep a balance between the amount of returns you will need regular access to and investments you can keep in place for longer periods of time. A middle ground example would be to invest in asset backed property developments, where you can negotiate monthly, quarterly or annual interest payments.

- What is your time horizon? Investors with longer time horizons, for example younger investors can generally afford to take on more risk, as they have more time to recover from short-term market volatility. Conversely, if you are older, or need liquidity or access to your investments in the short term, you might want to adopt a more conservative approach.

- How much volatility can you tolerate? High returns often come with high volatility. For example, investing in tech start-ups are seen high risk for the potentially high returns which can be as much as 100 x, depending on the business model. Assess how much fluctuation in your investment portfolio you are comfortable with, especially during market downturns.

- Do you have emergency funds? Having a liquid emergency fund separate from your investments can help you ride out market fluctuations without the need to sell investments at an inopportune time, especially if they are tied to specific terms. This helps reduce the psychological pressure to avoid risk altogether.

- What is your past experience with investing? Your level of comfort with different types of investments and your understanding of them can significantly affect your risk tolerance. Many investors backing property projects for example, are satisfied with knowing and trusting the people who are borrowing their money, however, it is important to understand their strategies, and delving into the numbers to ensure you also buy into their approach to successfully deliver, can help reassure you that the project is likely to benefit all parties, making the whole operation more viable.

By answering these questions, you can better understand your risk appetite and craft an investment strategy that aligns with both your financial goals and comfort level with risk.

The Importance Of Diversifying An Investment Portfolio

One of the most fundamental principles in wealth management is diversification. Diversifying your investment portfolio spreads your risk across different asset classes, sectors, and geographies, reducing your overall exposure to any single investment. The old adage "don’t put all your eggs in one basket" applies here.

Benefits of Diversification:

Risk Mitigation: If one asset class or sector performs poorly, gains in other investments can offset losses. For example, if the stock market drops, your investments in bonds or real estate may not be affected as severely.

- Improved Risk-Adjusted Returns: A diversified portfolio can achieve a higher return for the same amount of risk, or reduce risk for the same level of expected returns. This is achieved by combining assets with different risk and return profiles.

- Inflation Protection: Certain asset classes, like real estate or commodities, tend to perform well in inflationary environments, providing a hedge against the erosion of wealth. Meanwhile, stocks and bonds offer growth potential and income, respectively.

How to Diversify:

- Geographic Diversification: Spread investments across different countries and regions to avoid concentration risk from local economic conditions. While the UK market may be favorable, investing internationally can enhance returns and reduce country-specific risks.

- Sector Diversification: Instead of investing solely in one sector, such as technology or real estate, spread investments across various industries to mitigate sector-specific downturns.

- Asset Class Diversification: Invest in a mix of equities, bonds, real estate, private equity, and alternative investments such as commodities or cryptocurrencies. Each asset class behaves differently under various economic conditions. Even in the case of investing with property developers, its also sensible to invest in more than one company to spread the risks.

By diversifying, HNWIs can reduce risks, improve returns, and ensure that their wealth is more resilient in the face of market volatility and economic shifts.

Exploring Private Lending to Property Developers: A Unique Opportunity

One of the unique investment opportunities for HNWIs is private lending to property developers. In the UK, demand for rental accommodation continues to outstrip supply. This shortage of suitable rental homes presents a major opportunity for property developers to fill the gap, but many struggle to secure traditional financing through banks at a sustainable level, particularly during fast growth phases in their businesses, and when they are wanting to keep their leverage low by retaining a good portion of their own money in the game. Here, HNWIs can step in as private lenders, providing capital to developers in exchange for competitive returns.

The Current Rental Market in the UK

The UK rental market is currently experiencing a housing shortage, particularly in major cities like London, Manchester, and Birmingham. Rising property prices, the increasing population, an aging demographic, and economic factors are contributing to a growing demand for rental accommodation, particularly affordable homes. However, property developers often face barriers to accessing funding for new projects, as lending standards have tightened in recent years, particularly in the wake of the COVID-19 pandemic.

How Private Lending Works

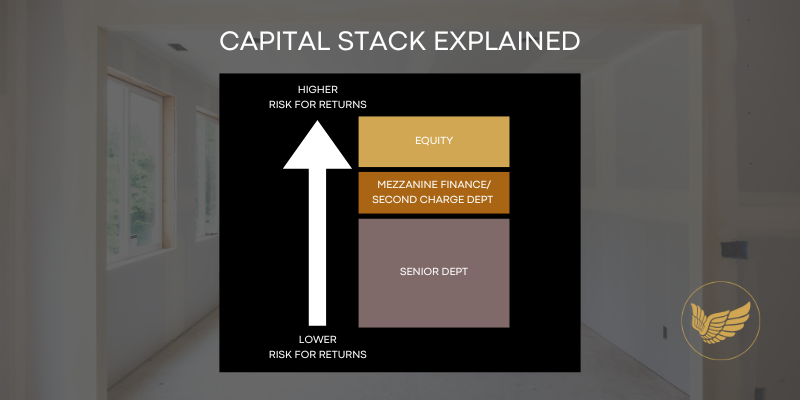

Private lending involves providing personal or business loans directly to property developers or developer-limited companies to fund their projects. These loans are usually short-term (12-36 months) and secured against the property being developed. In return for providing the loan, private lenders receive interest payments, typically at a rate higher than what traditional fixed-income investments, such as bonds, offer.

Benefits for HNWIs

- Attractive Returns: The interest rates on private loans to property developers tend to be higher than traditional fixed-income investments. Typical returns range from 6% to 12% per year, depending on the project's risk profile and the developer's track record.

- Asset-Backed Security: Since the loan is often secured against the property, there is a layer of protection for the investor. If the developer defaults on the loan, the lender can recover their investment by taking ownership of the property.

- Contributing to Social Good: By providing capital to developers, HNWIs are helping to address the housing shortage in the UK, particularly in the affordable rental market. This creates social impact by contributing to the supply of much-needed housing, especially for middle and lower-income renters.

Key Risks to Consider

- Developer Default: If the developer fails to complete the project or runs into financial difficulties, there is a risk of not receiving full repayment or any repayment on your loan. Conduct thorough due diligence on the developer’s track record, financial health, and the viability of the project.

- Market Conditions: Despite UK property showing a track record for being one of the most stable markets, it can still be volatile, and changes in property values can affect the viability of a development. A downturn in property prices, increasing cost of materials and trades work, can reduce the profitability of the project, which could impact loan repayment.

- Illiquidity: Private loans to property developers are not as liquid as stocks or bonds, meaning you may not be able to easily sell or exit the investment before the loan term ends.

Conclusion

For HNWIs, preserving and growing wealth requires strategic investing, a clear understanding of one’s risk appetite, and a well-diversified portfolio. Additionally, exploring alternative investments like private lending to property developers can provide attractive returns while contributing to the social good of addressing housing shortages in the UK. By considering risk, reward, and the overall market landscape, HNWIs can make informed decisions that help them maintain and grow their wealth over time.

By Helen turner

CREDITS

Written by Helen Turner, founder of PropertyAngels.Life - an initiative to accelerate the supply of adequate rental stock for the UK property market by helping high net worth individuals (HNWI) & sophisticated investors to find private lending and property investing confidence faster.

Go to the ABOUT page to read more on the initiative.

FOLLOW THE INITIATIVE

Step 1: Follow the initiative to watch it progress

Step 2: Receive your invite to join the ANGELS NETWORK to unlock access.

Top Picks

MORE ARTICLES