Private Lending Fuelling The BRRR (Buy, Refurbish, Refinance, Rent) HMO Industry

Synopsis From Thousands Of Appraisals

I have valued thousands of HMOs over the years. I mean thousands, too. What has been great about having this volume is that when I try to collate data or look at trends and cycles, there is a large sample pool to analyse. This allows me to get a really clear picture of not just what makes HMOs valuable or saleable, but also why landlords are choosing to sell in the first place.

The Results Make For Really Interesting Reading

Unlike any other property type, HMOs are notoriously transient. People tend to keep their homes for longer, and landlords hold onto their BTLs or commercial properties for longer, but there are some recurring issues within HMO ownership that trigger premature sales. I’ve been fascinated by this over many years.

So, What Factors Are At Play That Make HMOs Such A Transient Property Class?

First of all, it’s the fact that they are widely missold. “Quit your JOB with a high-yielding, hands-free investment,” “Cash-flowing, armchair investment,” or “Fully managed deal with guaranteed net returns.” The property education world has a lot to answer for here—the ‘get rich quick’ brigade that exploits the benefits that an HMO can provide over a BTL, for example, without really delving into the increased risks and the extra energy and time required to manage a well-functioning HMO asset.

It Doesn’t Sell Courses When Your Strapline Is, “Gain Better Returns By Working Harder.”

Some new HMO owners have found out the hard way that they couldn’t simply develop an HMO hundreds of miles away from where they live and expect a completely easy ride. This triggers some premature sales.

I also frequently spot ongoing management issues, tax changes, saturation concerns, ‘HMO fatigue,’ or a lack of lender support (down valuations, basically) as key factors that trigger premature HMO sales, and I could write extensively about any one of these with many case studies.

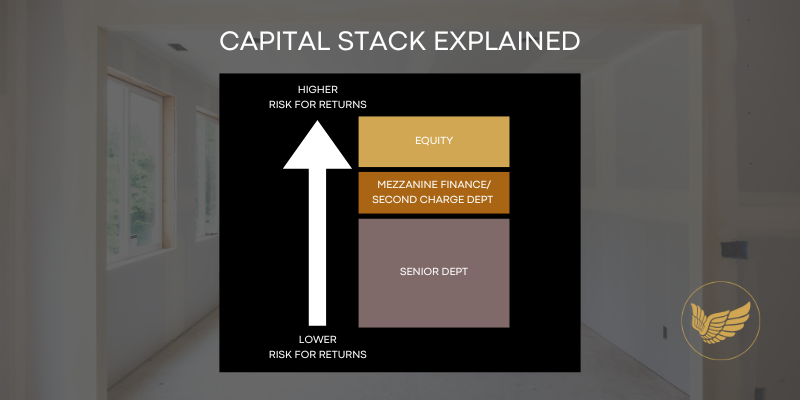

However, what I’m going to focus on here is perhaps the most common of them all: ‘JV (Joint Venture) Partner’ disagreements, splits, friction, or disasters. Business partner fallouts. Fixed-return lending mishaps and disasters.

'A huge portion of the HMO industry is propped up by ‘private lending’ or people rushing into JVs together, which, when it succeeds, can be the blueprint for creating many successful boutique HMOs and long-term business relationships. The issue is that the opposite is just as common.'

When most of the HMO advice on social media centres around creating highly leveraged BRRR properties using “none of your own money,” it’s no surprise that disasters are as common as successes. So, from my experience, what are the problems that lead to these disasters, and how can they be mitigated?

Would you rush into business with someone if they offered you a chance to buy a corner shop, a finance business, or a building contractor without any value add other than the money you’d be bringing to the table? No, you wouldn’t. You’d make damn sure that you did extensive due diligence on the proposal, reviewing the robust business accounts and future plans. If you didn’t fully understand it or feel completely confident, you probably wouldn’t invest.

When it comes to HMOs, however, private lenders (often extremely inexperienced) are somehow flocking to plough their hard-earned cash into BRRR HMO deals, often supporting inexperienced or not-so-liquid developers. In some cases, I use the word ‘developer’ very loosely.

Regardless of the relationship you have with the person asking for your money, and irrespective of the intentions and trustworthiness of the borrower, HMOs have pitfalls that even the most experienced can fall foul of. This bites hard if you didn’t expect it, there is no plan ‘B,’ or you need your cash back on time, as promised.

Simply Performing Due Diligence On The Individual Or Company And Trusting The Numbers Highlighted In Their Glossy ‘Investment Pack’ Isn’t Enough.

Ensuring that there are PGs in place, charges against assets, and proper, robust contracts securing your position isn’t enough either. If the numbers don’t stack, there’ll be no profits, and no profits could mean you don’t get your money back.

I’ve seen my fair share of investment packs, and they’re all brilliantly well-prepared. They include so much detail about the local area, the HMO market, and how this particular HMO development will be the best out there, with the highest rents, an amazing refinance, and a dream for all involved. The issue is, many are overly optimistic, completed naively, and rely solely on a grotesque refinance for you to get your money paid back.

It’s risky to borrow such huge sums of money when the pathway to paying it back is fraught with inconsistencies that are commonplace in the HMO planning, licensing, development, and refinancing landscape. None of these variables provide consistency, so how can the borrower be so confident?

A Little Over-Optimism In Each Area Can Be Catastrophic:

- Underestimating the timeframes

- Planning delays

- Build delays

- How that affects the cost of finance

- Lowballing the build costs and contingency

- Over-egging the expected rent roll

- Predicting too high of a commercial refinance

- Budgeting for a 10% yield and getting an 11% yield, for example

If issues like these arise, at best, the developer (borrower) can draw upon other assets and successful deals to cover the losses on any one deal. At worst, a developer may be tempted to bring in ‘new money’ constantly and effectively create a Ponzi scheme. We see it far too often.

Financial issues create cracks in relationships, and, getting back to the original point, when there are fast-tracked business relationships without concrete foundations, these cracks result in irreparable friction and damage. This leads to many more premature HMO sales.

If you want to support a brilliant HMO developer in their journey (I hate using that word!) and be one of the private investors who gets paid on time, it is crucial to think about each ‘deal’ and not just how well the borrower sells themself. Most developers are a couple of bad deals away from financial ruin, so your PGs, contracts, and charges mean nothing.

The Questions I'd Like To See Asked More:

- Does the borrower know enough about the local HMO market?

- Have they been in the industry long enough to go full cycle on several 3-5 year refinances?

- Do they manage successfully in the local area?

- Does the ‘deal’ stack? Are the room rates sustainable?

- What happens if there’s a down-valuation or a reduction in lender support?

- Does the borrower have potential delays covered, a large contingency, and a trusted local team with a track record of performing?

Do your own research on the local HMO market, the sold comparisons, the rents, and the viability of

what you’re being asked to invest in.

By Richard Nicholls

CREDITS

Richard Nicholls has been at the forefront of the HMO valuation and sales sector for many years and has worked with hundreds of landlords and thousands of HMOs across the UK.

He’s not just trying to ‘sell HMOs’ but create consistency and quality within the space and to provide knowledge and advice to HMO landlords and investors. In 2024 alone, Richard has visited and appraised over 400 HMOs.

FOLLOW THE INITIATIVE

Step 1: Follow the initiative to watch it progress

Step 2: Receive your invite to join the ANGELS NETWORK to unlock access.

Top Picks

MORE ARTICLES